SeaBank: automating everyday transfers with scheduled payments

SeaBank: automating everyday transfers with scheduled payments

SeaBank: automating everyday transfers with scheduled payments

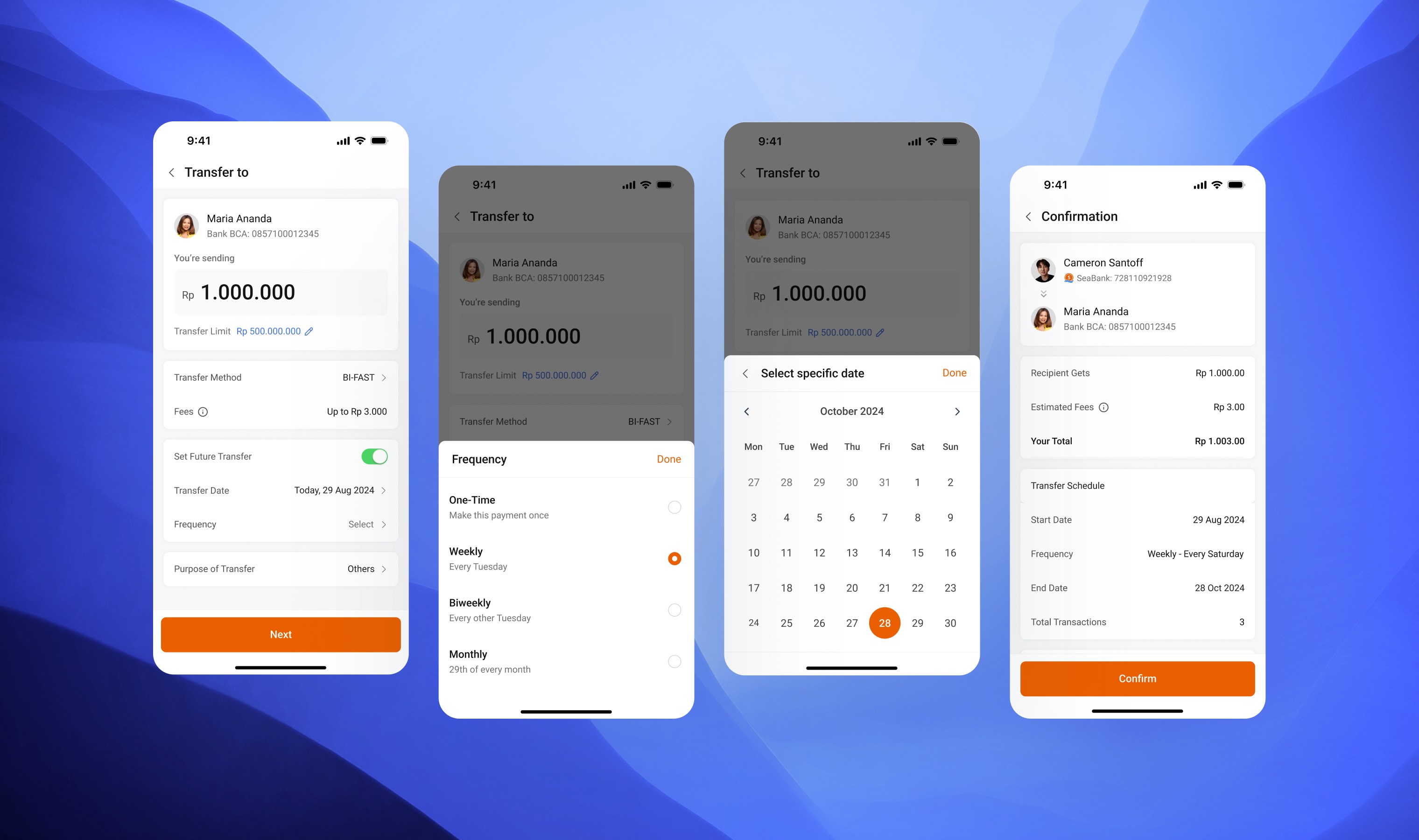

I led the design of a recurring transfer feature for SeaBank — enabling users to schedule automated transfers for fixed dates or intervals. This case covers how I integrated the new functionality into an existing money transfer flow, balancing flexibility and clarity for a wide range of financial literacy levels. The goal was to improve reliability for routine payments while maintaining trust and simplicity across a mobile-first user base.

I led the design of a recurring transfer feature for SeaBank — enabling users to schedule automated transfers for fixed dates or intervals. This case covers how I integrated the new functionality into an existing money transfer flow, balancing flexibility and clarity for a wide range of financial literacy levels. The goal was to improve reliability for routine payments while maintaining trust and simplicity across a mobile-first user base.

Role

Product designer

Product designer

Timeline

5 months

5 months

Team

Product Designers, Product Managers, Engineers and Business Development

Product Designers, Product Managers, Engineers and Business Development

What I worked on

Design exploration & prototyping

Cross-functional collaboration

Final design delivery and UAT

Design exploration & prototyping

Cross-functional collaboration

Final design delivery and UAT

SeaBank is a fast-growing digital bank in Indonesia, operated under SeaMoney — the financial services arm of Sea Group. With a mission to drive financial inclusion across Southeast Asia, SeaBank serves a wide range of underbanked individuals and micro-businesses.

Today, SeaBank supports hundreds of millions of users and processes millions of dollars in transactions daily.

SeaBank is a fast-growing digital bank in Indonesia, operated under SeaMoney — the financial services arm of Sea Group. With a mission to drive financial inclusion across Southeast Asia, SeaBank serves a wide range of underbanked individuals and micro-businesses. Today, SeaBank supports hundreds of millions of users and processes millions of dollars in transactions daily.

SeaBank: helping millions build better financial habits

SeaBank: helping millions build better financial habits

SeaBank: helping millions build better financial habits

Problem

Problem

While many users make regular payments, they have no efficient and reliable way to do so with SeaBank.

While many users make regular payments, they have no efficient and reliable way to do so with SeaBank.

“How might we help users quickly set up reliable repeat transfers — without disrupting their familiar flow?”

“How might we help users quickly set up reliable repeat transfers — without disrupting their familiar flow?”

“How might we help users quickly set up reliable repeat transfers — without disrupting their familiar flow?”

Outcome

Outcome

I delivered a streamlined recurring transfer experience that empowered users to automate personal transactions — such as family remittances, loan repayments, or employee disbursements. The solution drove repeat engagement, increased app retention, and aligned with our mission to support underserved users with tools for long-term financial control.

I delivered a streamlined recurring transfer experience that empowered users to automate personal transactions — such as family remittances, loan repayments, or employee disbursements. The solution drove repeat engagement, increased app retention, and aligned with our mission to support underserved users with tools for long-term financial control.

Discovery & Research

Discovery & Research

I partnered with out local research team to uncover:

I partnered with out local research team to uncover:

85%

85%

of SeaBank users make regular transfers

of SeaBank users make regular transfers

Most users move money on a weekly or monthly basis.

Most users move money on a weekly or monthly basis.

56%

56%

of those transfers are to non-unique recipients

of those transfers are to non-unique recipients

Users often send to the same people repeatedly.

Users often send to the same people repeatedly.

43%

43%

of users use recurring transfer features on other apps

of users use recurring transfer features on other apps

These transfers are often for essential purposes — family support, instalments, and investments.

These transfers are often for essential purposes — family support, instalments, and investments.

Business Goals

Business Goals

#1

Increase transfer frequency with a target of +1.2x monthly transfers per user

Increase transfer frequency with a target of +1.2x monthly transfers per user

#2

Improve feature retention — by tracking repeat usage

Improve feature retention — by tracking repeat usage

#3

Stay competitive — most major players in the market already offer this feature

Stay competitive — most major players in the market already offer this feature

Mapping User Needs

Mapping User Needs

#1

Peace of mind — Fewer forgotten payments, less mental load

Peace of mind — Fewer forgotten payments, less mental load

#2

Reliability — Confirmed success states, clear and trustworthy UI

#3

Simplicity & Convenience — From setup to managing recurring transfers

Simplicity & Convenience — From setup to managing recurring transfers

Competitor Benchmarking

Competitor Benchmarking

Partnered with local market research teams to evaluate scheduled transfer features across 8 top digital financial services in Indonesia. These gaps highlighted a clear opportunity for us to stand out:

Partnered with local market research teams to evaluate scheduled transfer features across 8 top digital financial services in Indonesia. These gaps highlighted a clear opportunity for us to stand out:

Limited frequency options

Limited frequency options

Most apps only offered basic settings like weekly or monthly.

Most apps only offered basic settings like weekly or monthly.

Editing limitations

Editing limitations

Only half of competitors let users modify their scheduled transfers.

Only half of competitors let users modify their scheduled transfers.

Lack of reminders

Lack of reminders

Very few apps offered proactive notifications before a scheduled transfer.

Very few apps offered proactive notifications before a scheduled transfer.

Design Principles

Design Principles

To guide our solutions, we established four key design principles. These helped ensure the feature was not just functional — but usable, flexible, and trustworthy.

To guide our solutions, we established four key design principles. These helped ensure the feature was not just functional — but usable, flexible, and trustworthy.

#1

#1

🔁 Fast Familiarity

🔁 Fast Familiarity

Users shouldn't have to relearn how transfers work. Any added feature must feel like a natural extension of existing behaviors.

Users shouldn't have to relearn how transfers work. Any added feature must feel like a natural extension of existing behaviors.

#2

#2

🎛️ Flexible Config

🎛️ Flexible Config

Users have diverse needs — from sending salaries to paying family. Design should adapt without adding bloat.

Users have diverse needs — from sending salaries to paying family. Design should adapt without adding bloat.

#3

#3

📉 Minimize Drop-off

📉 Minimize Drop-off

Guide users through the flow with zero dead ends.

Friction = abandonment.

Guide users through the flow with zero dead ends.

Friction = abandonment.

#4

#4

🥃 Transparent State

🥃 Transparent State

Users must feel in control. They should always know what's scheduled, what’s coming next, and what can be changed.

Users must feel in control. They should always know what's scheduled, what’s coming next, and what can be changed.

Choosing the Right Interaction Model

Choosing the Right Interaction Model

Before designing the UI, we had to understand how users mentally approach transfers. This meant identifying the right flow model — one that aligns with how people actually think and behave. I explored two models:

Before designing the UI, we had to understand how users mentally approach transfers. This meant identifying the right flow model — one that aligns with how people actually think and behave. I explored two models:

Usability Testing & Iterations

Usability Testing & Iterations

To validate the design, we partnered with the local UX research team for moderated sessions in Jakarta, indonesia. This approach combined quantitative and qualitative insights, allowing us to measure performance and understand user sentiment.

To validate the design, we partnered with the local UX research team for moderated sessions in Jakarta, indonesia. This approach combined quantitative and qualitative insights, allowing us to measure performance and understand user sentiment.

Sample Size

Sample Size

20–30 users per key user segment

Urban digital-savvy

Rural users (lower tech familiarity)

Small business users

20–30 users per key user segment

Urban digital-savvy

Rural users (lower tech familiarity)

Small business users

Languages

Languages

Prototypes fully translated into Bahasa

Copy QA’d with local content team

Moderated by native speakers trained in usability observation

Prototypes fully translated into Bahasa

Copy QA’d with local content team

Moderated by native speakers trained in usability observation

Tasks

Tasks

Scenarios reflected cultural use cases, e.g. payday family support)

Scenarios reflected cultural use cases, e.g. payday family support)

Iteration #1 – Clarifying Frequency Options

Iteration #1 – Clarifying Frequency Options

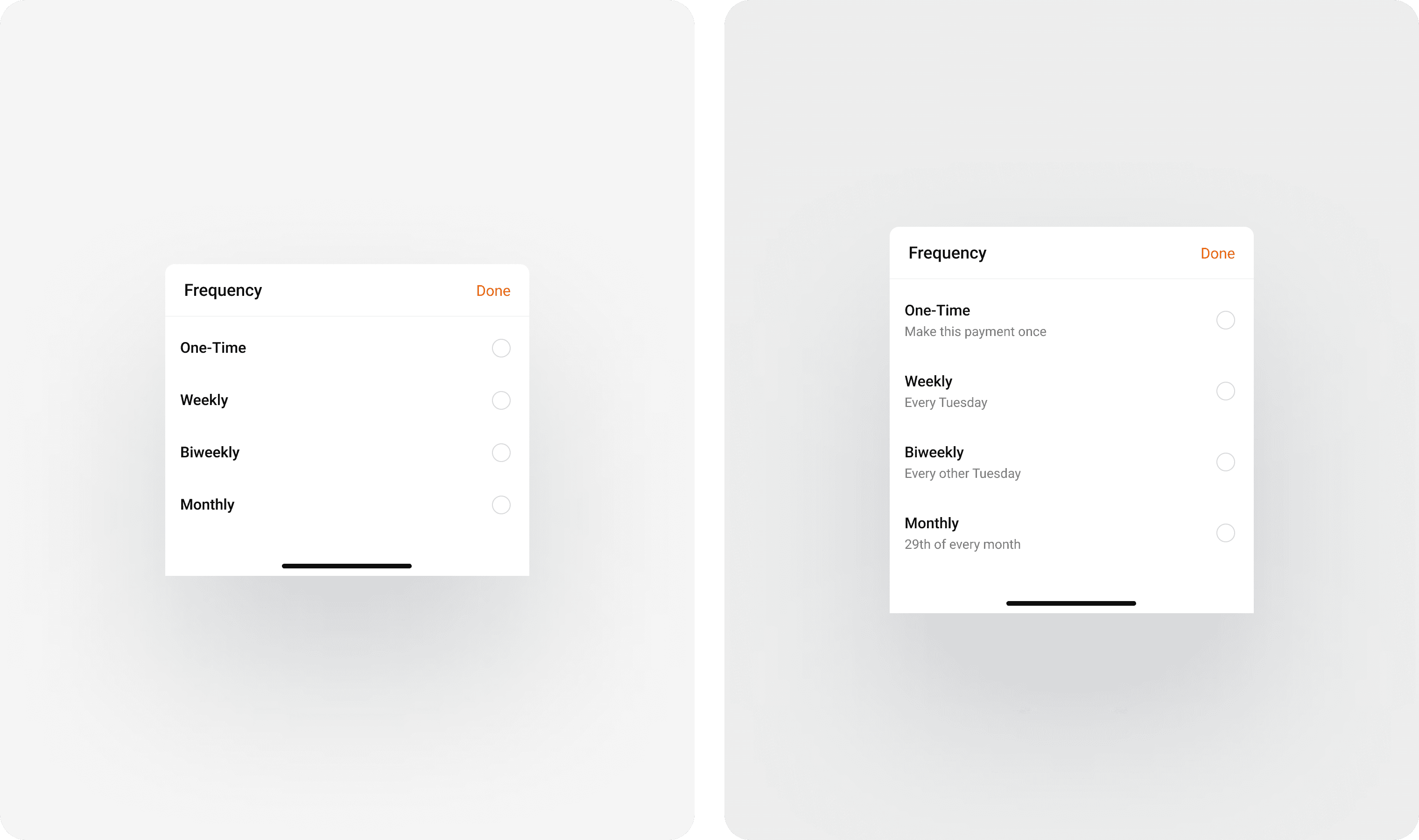

Users, especially in rural segments, didn’t fully understand the difference between options like "Biweekly" and "Monthly." Some assumed “Monthly” meant the same date each month, while others thought it meant every four weeks.

Users, especially in rural segments, didn’t fully understand the difference between options like "Biweekly" and "Monthly." Some assumed “Monthly” meant the same date each month, while others thought it meant every four weeks.

We introduced contextual subtext below each label to spell out what would happen. This reduced hesitation and gave users immediate, date-specific clarity.

We introduced contextual subtext below each label to spell out what would happen. This reduced hesitation and gave users immediate, date-specific clarity.

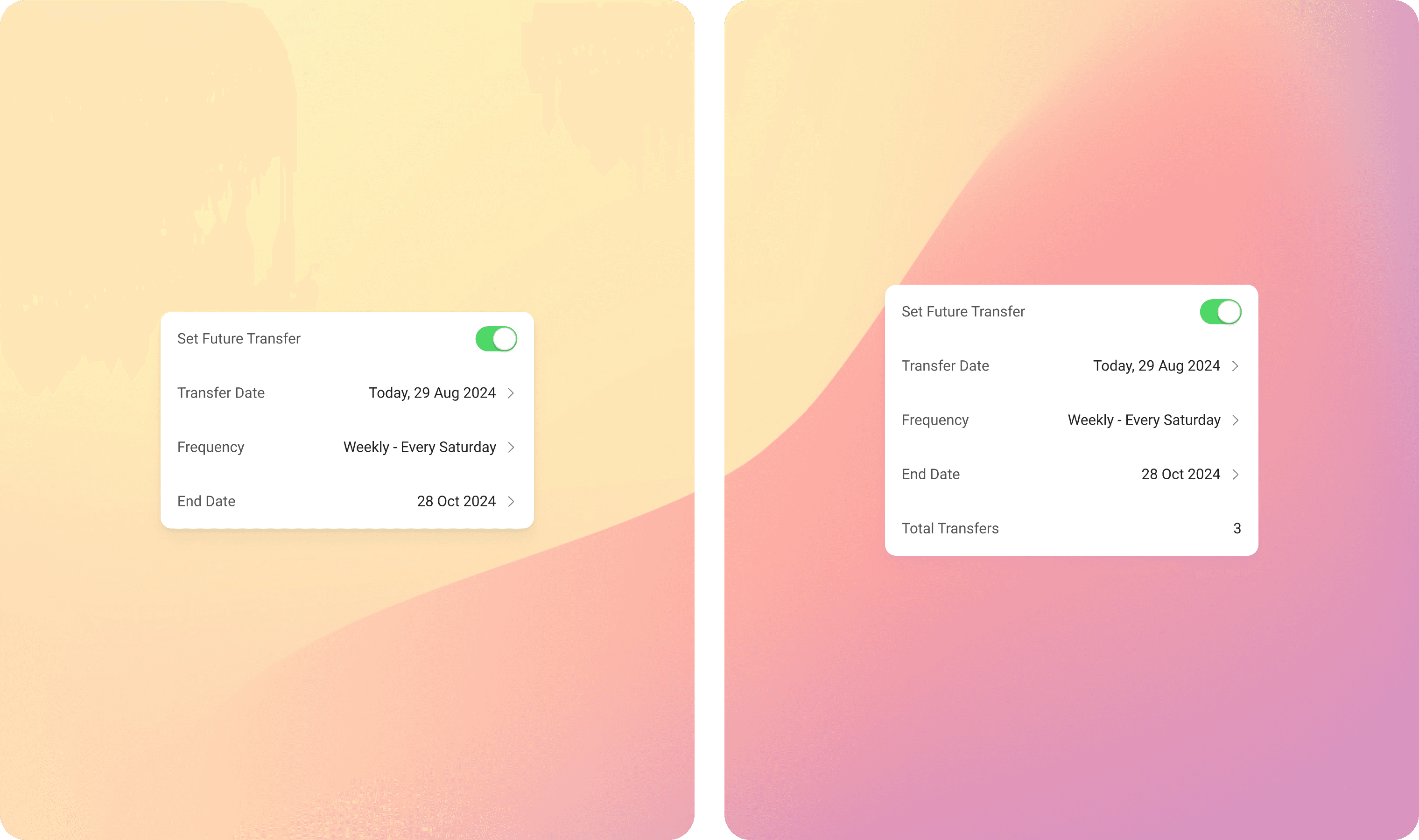

Iteration #2 – Providing a Clearer Sense of Control with End Dates

Iteration #2 – Providing a Clearer Sense of Control with End Dates

Some users were anxious about not knowing how many payments would go through.

Some users were anxious about not knowing how many payments would go through.

We added a dynamic field labeled Total Transfers, which appears when users define an end date. This gives them an exact count of how many payments will occur.

We added a dynamic field labeled Total Transfers, which appears when users define an end date. This gives them an exact count of how many payments will occur.

Iteration #3 – Surfacing Date Logic for Edge Cases

Iteration #3 – Surfacing Date Logic for Edge Cases

Originally, logic for handling unavailable dates like the 31st was hidden in an info icon. Some users raised questions and a minority abandoned the flow when they weren’t sure.

Originally, logic for handling unavailable dates like the 31st was hidden in an info icon. Some users raised questions and a minority abandoned the flow when they weren’t sure.

We decided to surface this information directly in-line as a short explanatory note. By surfacing the logic directly, we eliminated confusion and boosted trust.

We decided to surface this information directly in-line as a short explanatory note. By surfacing the logic directly, we eliminated confusion and boosted trust.

Final Solution

Final Solution

The final design embedded recurring transfer setup directly into the existing money transfer flow. Users could choose a frequency (daily, weekly, monthly), define an end condition, and review a clear summary before confirming. The design focused on progressive disclosure — surfacing options only when needed — while maintaining clarity, reducing error risk, and ensuring transparency around future deductions.

The final design embedded recurring transfer setup directly into the existing money transfer flow. Users could choose a frequency (daily, weekly, monthly), define an end condition, and review a clear summary before confirming. The design focused on progressive disclosure — surfacing options only when needed — while maintaining clarity, reducing error risk, and ensuring transparency around future deductions.

Results & impact

Results & impact

Here’s what we saw after rollout, 6 months post-launch:

Here’s what we saw after rollout, 6 months post-launch:

27%

27%

of active users adopted scheduled transfers

of active users adopted scheduled transfers

Of those, 61% repeated it — showing behaviour stickiness

Sales teams think in buyer intent; data teams think in statistical signals. We needed to bridge the gap between technical logic and sales narrative.

18%

18%

increase in average monthly transfers per feature user

increase in average monthly transfers per feature user

73%

73%

of users kept the reminder notifications ON

of users kept the reminder notifications ON

A strong signal of perceived value

12%

12%

of users exercised control

of users exercised control

Scheduled transfers were being edited or/and cancelled